The Rise of the Fast Money Generation

Millennials and Gen Z—those born from 1981 to 2012—are the first generations since the 1800s projected to be worse off than their parents. Data increasingly shows that today’s young adults report lower levels of happiness and well-being than previous generations, driven by economic pressures and the omnipresence of social media.

The Social Media Effect: Fuel to the Fire

Social media acts as an accelerant for this generations’ challenges. In an era where content is created and consumed 24/7, curated digital identities are constantly on display. No lifestyle, trend, or aesthetic is out of reach—or out of comparison. The result is a heightened sense of inadequacy and a constant pressure to "keep up with the Joneses," now scaled globally and algorithmically.

User-generated content—often filtered, exaggerated, or outright false—creates a distorted reality. As traditional forms of entertainment become increasingly expensive (think movie theaters, sporting events, arcades), social media offers an accessible, low-cost alternative that provides both stimulation and social validation. But it comes at the cost of self-worth and mental well-being.

Economic Anxiety: A Generation Left Behind

The economic anxieties are not imagined—they are measurable and profound. Baby Boomers hold an estimated $76 trillion, or 52% of all U.S. wealth, while comprising only 20% of the population. When it comes to home ownership—a foundational asset for building wealth—the contrast is stark: only 33% of 27-year-olds today own a home, compared to 40% of Boomers at the same age. The issue isn’t a lack of aspiration; it’s affordability.

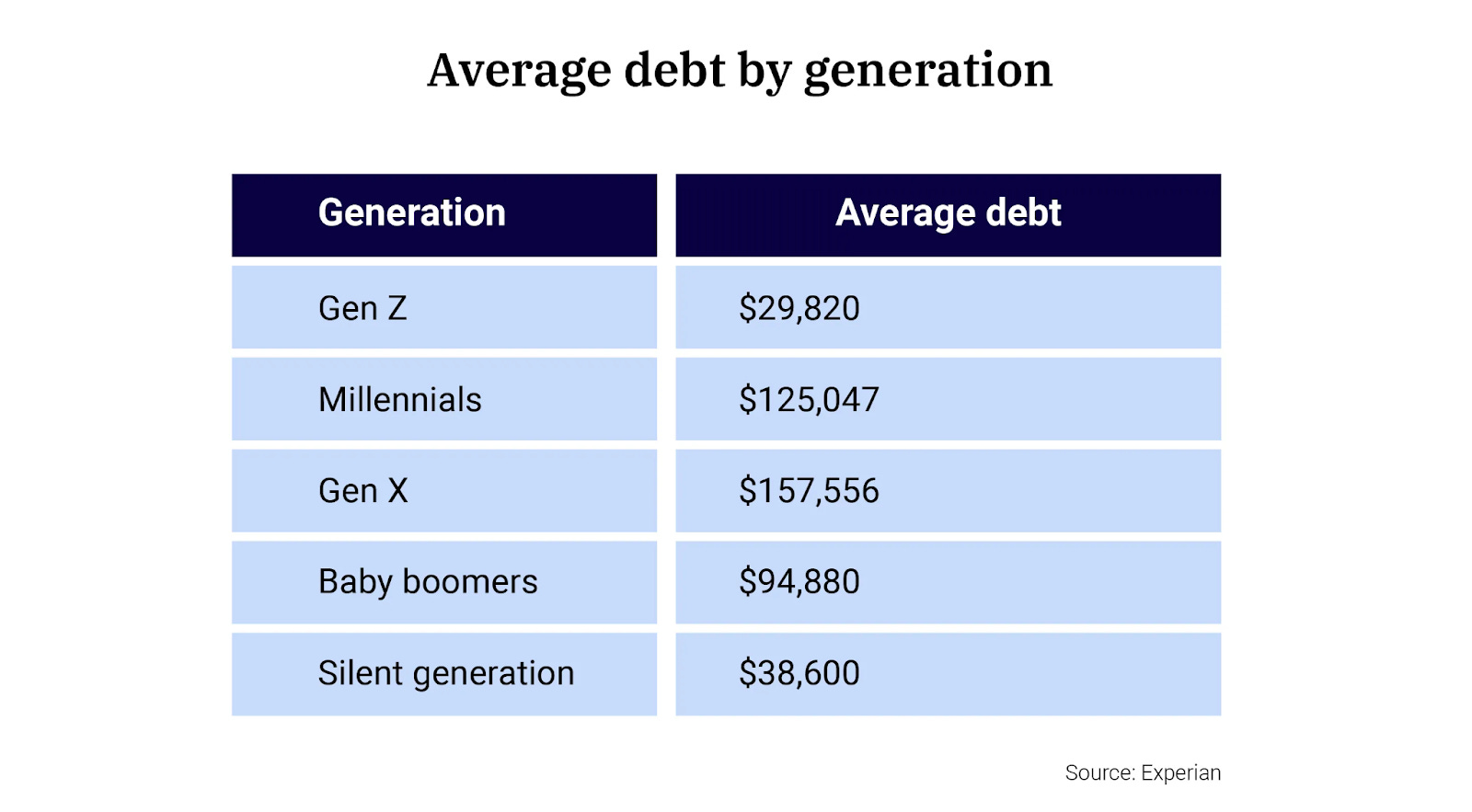

Meanwhile, debt levels have ballooned. The financial starting line for younger generations is significantly farther back than it was for their parents.

Fast Money: Risk as Identity

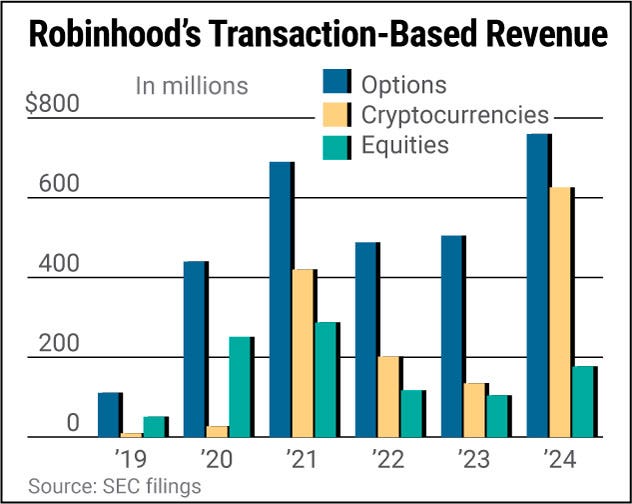

In response to these conditions, a new ethos has emerged—what might be called the Fast Money Generation. Faced with slower wage growth and fewer traditional pathways to wealth, younger Americans are increasingly drawn to high-risk, high-reward ventures. There are over 80 million videos on YouTube about making money, many of which are get rich quick schemes. This mentality is reflected in the explosion of day trading apps like Robinhood and Webull, which make stock trading feel more like a game than a financial decision. You add in the ability to use leverage and play the options market literally creates a casino for them. In 2020 alone, Robinhood added more than 3 million users, many of them first-time investors.

Crypto, NFTs, and memecoins like $DOGE and $TRUMP became cultural phenomena—part investment, part meme, part rebellion. A survey by Pew Research found that 43% of men aged 18 to 29 have invested in, traded, or used cryptocurrency. Meanwhile, prediction markets and sports betting have moved from the fringes to the mainstream. Companies like DraftKings and FanDuel have normalized gambling as entertainment, and prediction markets like Polymarket and Kalshi are blending finance with forecasting in ways never before imagined.

These tools are more than just financial instruments—they are identity platforms. People showcase their wins, meme their losses, and build audiences around the rollercoaster of risk. For many, the logic is simple: if traditional wealth-building is slow, exclusive, and uncertain, then why not gamble for a chance to leap ahead?

Innovating Our Way Out?

There’s growing conversation around our entry into the Age of Abundant Intelligence. Just as the industrial era and the rise of machines reduced the need for physical labor and elevated quality of life, could artificial intelligence do the same for cognitive labor?

If AI can lower the average amount of productive work required per person—while maintaining or even increasing GDP—we may be on the brink of a profound societal shift. This could empower the Fast Money Generation to create more income with less time, while also reducing the cost of goods, services, and even education.

In this optimistic scenario, technology doesn't just replace effort—it amplifies opportunity. If we can harness this potential wisely, it may help rebalance the economic scales and offer the Fast Money Generation not just a fighting chance, but a future of abundance, agency, and renewed hope.